Getting approved for an auto loan refinance is not just about having a good credit score. Lenders run a structured risk assessment on every application, and a strong score can still get declined if the vehicle value is too low or the monthly debt load is too high.

For the calculator and full refinance tools, visit the Auto Loan Refinance Calculator

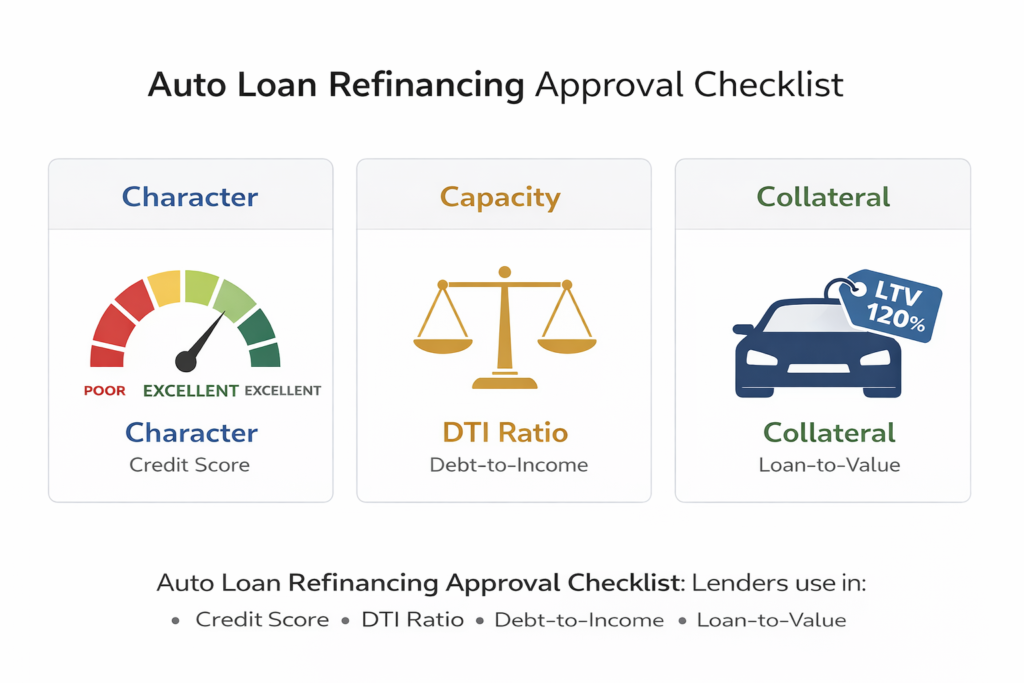

The Mechanics of Lender Risk Assessment

Underwriters look at three factors in combination: the car itself (collateral), your ability to pay (capacity), and your payment history (character). A weakness in any one of them can outweigh strength in the others. Understanding how lenders weight these factors is the most practical thing you can do before applying.

Loan-to-Value Ratios: The Most Critical Barrier

LTV is usually the first thing an underwriter checks, and it is the most common reason refinance applications are declined before anything else is even reviewed.

LTV=(Current Vehicle ValueTotal Loan Amount)×100

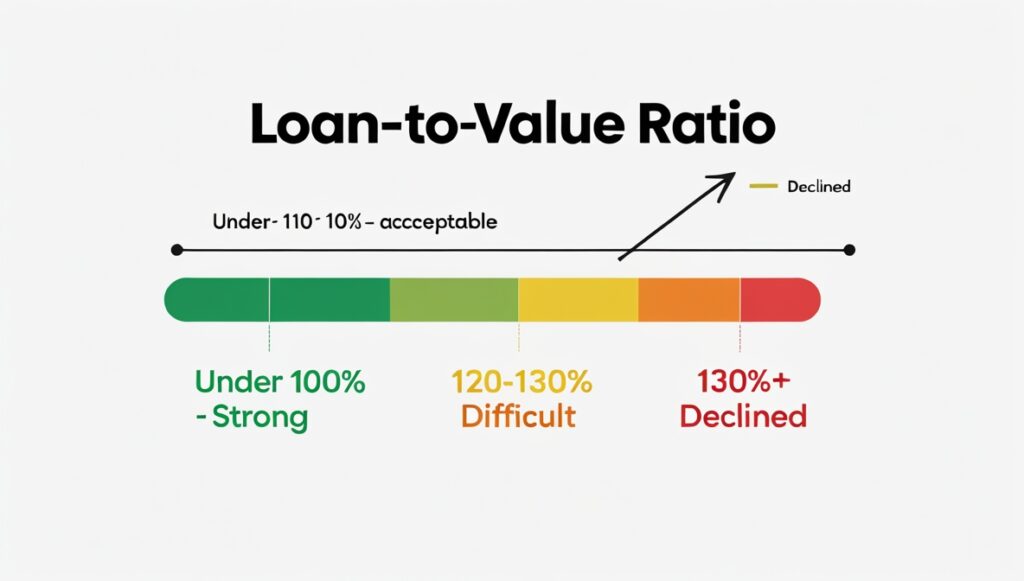

Most lenders set maximum LTV limits. A common cap is 120 percent. That means they will finance up to 20 percent above the car value to cover taxes and fees. If your LTV is higher, you might be denied.

Why LTV matters

The lender’s concern is straightforward: if you default, they repossess the car and sell it to recover the loan balance. If you owe more than the car is worth, they take a loss. Most lenders cap refinances at 120% LTV for exactly this reason.

Practical fix for high LTV

If your LTV is too high, the three practical options are: make a lump-sum cash payment to bring the balance down, wait until regular payments reduce the balance to an acceptable level, or find a lender with a higher LTV tolerance, which typically requires a strong credit profile to offset the collateral risk.

Case Study: Sarah’s Negative Equity Challenge

Sarah has a 2022 SUV valued at $18,000. She owes $23,500.

Calculate LTV: (23,500 / 18,000) × 100 = 130.5 percent.

Most lenders cap at 120 percent. To reach 120 percent, the maximum loan allowed is 1.20 × 18,000 = $21,600. Sarah must lower her balance from $23,500 to $21,600. That means a one-time cash payment of $1,900 to qualify.

This cash-in option is common. It reduces lender risk and gives the borrower access to lower rates.

Debt-to-Income (DTI) Thresholds

DTI measures whether you have enough monthly income left over after existing debt payments to handle a new loan. Lenders calculate it by dividing your total monthly debt obligations by your gross monthly income.

At 50% DTI, half your pre-tax income goes to debt payments before rent, food, or anything else. Most lenders treat anything above 45% as high risk. The target range is 35 to 45%, and prime borrowers with low LTV can sometimes go higher.

One thing worth knowing: refinancing to a lower monthly payment actually improves your DTI. If your current payment is $520 and the new payment is $465, your monthly debt load drops by $55, which may move you into a better approval band. Run the calculator first to see what your new payment would be, then factor that into your DTI estimate.

Vehicle Eligibility and Restrictions

The vehicle itself has to pass a separate eligibility check before the lender even looks at your finances. Most standard passenger cars qualify, but lenders apply restrictions based on age, mileage, and title status.

The most common hard cutoffs are 10 years old or newer and under 100,000 to 120,000 miles. Vehicles with salvage or rebuilt titles are almost universally ineligible because their resale value is unpredictable. Cars used for rideshare or commercial purposes often need a specialized program.

If your vehicle is borderline on age or mileage, call the lender directly before submitting a formal application. A soft inquiry or phone call costs nothing. A hard inquiry that leads to a denial temporarily affects your credit score.

Documentation Checklist

A clean file speeds approval. Typical documents underwriters want:

- Proof of Income. The recent 30 days of pay stubs or two years of tax returns for the self-employed.

- Proof of Residence. Recent utility bill or lease.

- Proof of Insurance. Full coverage with acceptable deductibles.

- Current Payoff Statement. A 10-day payoff showing the exact payoff amount.

- Title and Registration. Clear title with no liens that conflict.

- Odometer Disclosure. Current mileage reading.

- Photo ID. Driver’s license or state ID.

- Bank Statements. The past 1 to 3 months to verify cash flow.

Provide clear, dated documents. Incomplete or inconsistent files trigger manual review and delays.

Table: Common Approval Tiers by Credit Score

| Credit Tier | Score Range | Typical Max LTV | DTI Requirement |

|---|---|---|---|

| Super Prime | 740+ | 125% – 130% | Up to 50% |

| Prime | 680 – 739 | 120% | Under 45% |

| Near Prime | 620 – 679 | 110% | Under 40% |

| Subprime | Under 620 | 100% (No Negative Equity) | Under 35% |

These bands vary by lender and program. Use them as a rough map, not a guarantee.

Why Lenders Require a Hard Credit Pull

Pre-qualification often uses a soft pull. It gives a rate estimate without affecting your score. Final underwriting uses a hard inquiry. The lender needs the full credit file and recent trade activity. A hard pull shows:

- Recent late payments.

- Collection accounts.

- New closed accounts or bankruptcies.

- The full exposure from other loans and cards.

Underwriters want to see at least 24 months of payment history. A 30-day late on the current car loan can be disqualifying for many programs. Manual underwriters may make exceptions, but automated systems often decline on this signal.

Manual vs Automated Underwriting

Some loans go through automated systems. These systems apply score and ratio rules quickly. Others get a manual review. Manual underwriting can allow exceptions. It can accept compensating factors such as:

- Recent steady employment.

- Large savings or assets.

- A strong payment history on other loans.

If you have borderline numbers, request a manual review. Provide documentation that shows stability.

Final Strategy for Approval

The most effective thing you can do before applying is run through the same checklist an underwriter will use. Check your vehicle’s current market value on Kelley Blue Book or NADA using the private party figure, which is what lenders use for LTV calculations. Pull your own credit report and dispute any errors before a lender sees them. Calculate your DTI using your real monthly debt obligations, not an estimate.

Get a formal 10-day payoff quote from your current lender so you have the exact balance, not the approximate figure from your last statement. If your LTV is above 120%, decide whether a cash-in payment to bring it down is worth the access to better rates.

When you are ready to shop, use soft pre-qualification wherever it is available. Most online lenders offer this. It lets you compare rates across multiple lenders without triggering hard inquiries on every application. If you do get declined, ask for the specific reason in writing. Most of the common denial factors can be addressed over time.

Disclaimer: Underwriting criteria vary by lender. This article is for educational purposes and does not guarantee loan approval