A car loan has three moving parts: Principal, APR, and Time. The principal is the money you borrow. The APR is the yearly cost of borrowing. Time is how many months you take to pay. Monthly interest equals APR divided by 12, applied to the outstanding balance each month. The monthly payment stays the same for fixed-rate loans. The payment splits each month into an interest portion and a principal portion.

For the main calculator and all resources, visit Auto Loan Refinance Calculator

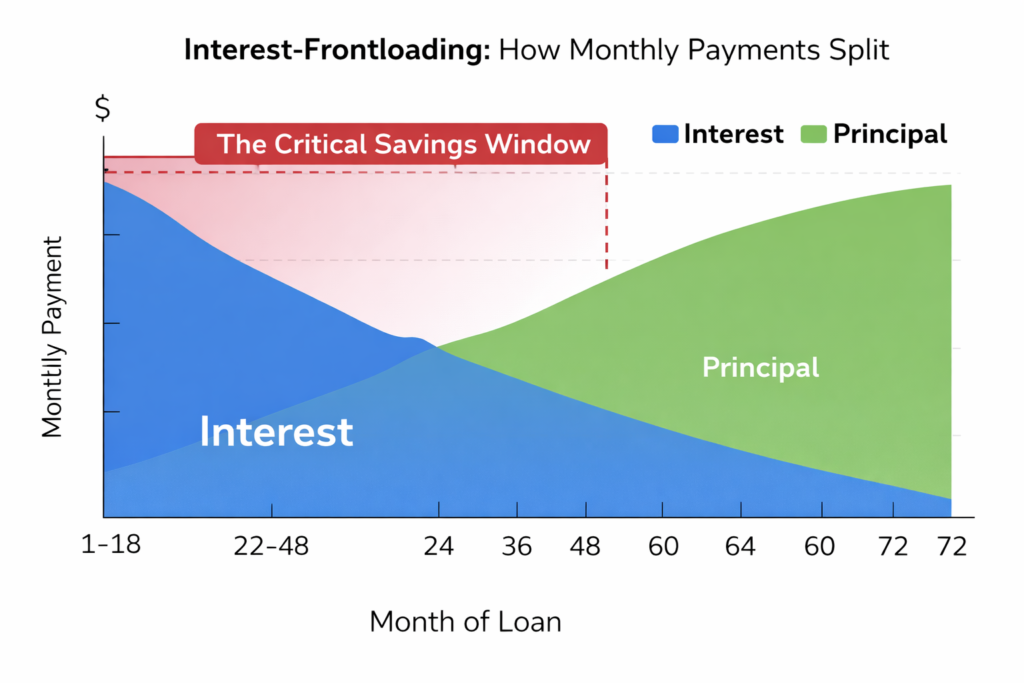

Auto loans are front-loaded with interest because of how amortization formulas split each monthly payment. At the start, the outstanding balance is highest. Interest is a percent of that balance. Lenders compute interest on each monthly balance before subtracting the principal portion. That makes the first payments pay mostly interest and only a small slice of principal. Over time, as the principal shrinks, the interest slice gets smaller, and the principal slice grows. This pattern is not a trick. It is the math of fixed payment loans. Lenders also charge interest on fees added to the loan, which increases the balance you pay interest on. Monthly interest uses the beginning balance for that month. If you miss or defer payments, unpaid interest can compound and push more of your future payments to interest. Because early payments pay little principal, it takes many months before you lower the balance enough to see large principal gains. That is why paying extra principal early or refinancing to a lower rate changes the schedule fast. Finally, longer loan terms slow principal paydown. A longer term keeps monthly payments low, but it also keeps the early-interest-heavy phase longer. Small extra payments early make a large difference.

The Master Formula

The standard monthly payment formula is:M=P⋅(1+i)n−1i(1+i)n

Where M is the monthly payment, P is principal, i is the monthly interest rate (APR / 12), and n is the number of months.

If i change by 0.5 percentage point in APR, the monthly i changes by 0.005/12. That small change alters M and the total interest.

Example using P = $25,000, n = 60:

Monthly payment at 6.0% APR: $483.32.

Monthly payment at 6.5% APR: $489.15.

The monthly payment rises by $5.83 (about 1.21 percent). Over 60 months, the total interest rises from $3,999.20 to $4,349.22. That is $350.02 more interest across the loan for a 0.5 percentage point increase.

This shows why even half a percent matters. The math compounds across many months.

Simple Interest vs. Precomputed Interest

Simple interest loans calculate interest only on the outstanding principal each day or month. You are charged interest on what you actually owe. If you pay extra principal or pay early in a month, you reduce future interest right away.

Precomputed interest (add-on interest) calculates total interest at the start, then adds it to the principal and divides by the number of months. That method charges interest on the full original balance for the whole term, even as the loan balance falls. It gives a higher effective cost to the borrower.

Daily accrual under simple interest means interest = (annual rate / 365) times daily balance, summed over days between payments. That is fairer. Precomputed methods lock you into an interest rate that does not fall as your balance falls. For consumer protection, simple interest is generally better.

The Rule of 78s: A Hidden Risk

While most modern auto loans use simple interest, some “subprime” or older lenders still use a method called the Rule of 78s. This is a precomputed interest method that heavily weights interest charges toward the beginning of the loan. If your current loan uses this method, refinancing mid-term might not save you as much as the math suggests because you’ve already paid the bulk of the interest. Before using our calculator, check your original loan agreement for the phrase “Rule of 78s” or “Precomputed Interest.”

High Interest Trap

For Example, Marcus bought a car and borrowed $25,000 at 14.0% APR for 60 months. He made on-time monthly payments of $581.71. In the first six months, his payments break down as follows.

14.0% scenario, monthly payment $581.71:

| Month | Beginning Balance | Interest Paid | Principal Paid | Ending Balance |

|---|---|---|---|---|

| M1 | $25,000.00 | $291.67 | $290.04 | $24,709.96 |

| M2 | $24,709.96 | $288.28 | $293.42 | $24,416.54 |

| M3 | $24,416.54 | $284.86 | $296.85 | $24,119.69 |

| M4 | $24,119.69 | $281.40 | $300.31 | $23,819.38 |

| M5 | $23,819.38 | $277.89 | $303.81 | $23,515.57 |

| M6 | $23,515.57 | $274.35 | $307.36 | $23,208.21 |

After six months at 14%, Marcus has paid $1,791.79 toward principal and $1,698.45 in interest. He refinances to 6.0% APR. The new monthly payment becomes $483.32.

6.0% scenario, monthly payment $483.32:

| Month | Beginning Balance | Interest Paid | Principal Paid | Ending Balance |

|---|---|---|---|---|

| M1 | $25,000.00 | $125.00 | $358.32 | $24,641.68 |

| M2 | $24,641.68 | $123.21 | $360.11 | $24,281.57 |

| M3 | $24,281.57 | $121.41 | $361.91 | $23,919.66 |

| M4 | $23,919.66 | $119.60 | $363.72 | $23,555.93 |

| M5 | $23,555.93 | $117.78 | $365.54 | $23,190.39 |

| M6 | $23,190.39 | $115.95 | $367.37 | $22,823.03 |

After six months at 6%, Marcus has paid $2,176.97 of principal and $722.95 in interest. That is an extra $385.18 of principal paid compared with 14%, and $975.50 less interest in those six months. The refinance lowers his bill and shifts much more of each payment to principal. Marcus used the savings to build a small buffer. He kept the same term, so the loan length did not change. His case shows how a high rate traps you. A lower rate frees cash and reduces interest fast. Refinancing is not automatic; factor in fees, credit score, and lender terms before you decide. And compare the total cost over life.

The Amortization Table Breakdown

Every amortization row has four key columns:

Beginning Balance shows what you owe at the start of the period.

Interest Paid is the interest charged for that period. It equals beginning balance times the monthly rate.

Principal Paid equals the fixed payment minus interest. It reduces the balance.

Ending Balance is the beginning balance minus the principal paid. It becomes the next period’s beginning balance.

Read any row left to right. Early rows show high interest and small principal. Later rows invert that.

Negative Amortization Risk

If you defer or skip payments, unpaid interest can be added to the balance. That raises the principal. When the principal grows, future interest grows too. This is negative amortization. It means your balance can rise even while you make payments. Always check whether a loan allows deferred payments or capitalized interest. Those terms increase long-term cost.

Calculation Accuracy and Local Fees

The Total Loan Amount is not only the car price. It can include taxes, title fees, dealer fees, and gap or service contracts. States set title and registration fees. For example, Nevada and New York use different fee schedules. If Nevada has a lower title fee than New York, the loan amount differs even for the same car. Lenders compute interest on the fully financed amount. That is why local fees matter. Always add state fees to the loan numbers when you run an amortization.

Differences in State-Level Accrual Logic

While the amortization formula is a mathematical constant, how lenders apply it can vary based on state regulations. For example, some states allow for “Force-Placed Insurance” or specific “Lien Filing Fees” to be rolled into the principal ($P$) mid-loan.

Furthermore, the distinction between a 360-day year (often used in commercial banking) and a 365-day year (standard for consumer auto loans) can create a 1.3% variance in the interest accrued over the life of the loan. When performing a manual audit of your amortization table, always confirm which day-count convention your lender utilizes.

Methodology Summary

Our calculator utilizes the standard fixed-rate amortization formula:

By focusing on the Principal ($P$) and the Monthly Interest Rate ($r$), we provide a projection of your debt lifecycle. However, users should remember that car loans are amortized daily. This means that the exact day your payment reaches the lender can cause a minor variance in the interest charged for that month. To ensure 100% accuracy in your refinance planning, we recommend requesting a 10-day payoff statement from your current lender to get the exact $P$ value for your calculation.